2.1 Tourist accommodation in Switzerland

2020 and 2021 were marked both nationally and internationally by the health and economic crisis linked to the COVID–19 pandemic. The various measures taken by Switzerland and foreign states have had a direct influence on the tourism sector as a whole and more particularly on the tourist accommodation sector. The statistical results for 2021 reflect the negative effects of this exceptional situation on this sector often with very "extreme" values that have never been seen in the past. It is not possible to list measures taken at international level. However, a chronology of the measures taken in Switzerland provides a relevant context for the interpretation of the results.

Timeline:

2020

End

of February: The Federal Council declares Switzerland as being in a "special situation". Events, conferences and seminars are cancelled for the first time.

March: The Federal Council declares an “extraordinary situation". The partial lockdown starts. Restaurants, shops, markets, leisure facilities and businesses where distance rules cannot be respected must close. However hotels remain open. Border checks are enforced with all neighbouring countries.

May: Easing of some health measures. Shops, compulsory schools, museums, libraries, restaurants and sports halls can gradually reopen but with strict health protection measures.

June: The Federal Council puts an end to the extraordinary situation. Leisure facilities and other tourist attractions can reopen. Spontaneous gatherings of up to 30 people are allowed again and demonstrations of up to 300 people can be organised. Restrictions on entry into Switzerland are lifted for all Schengen states.

October –

November: Start of the second "wave" of COVID-19. Progressive reintroduction of cantonal and federal health measures.

December: The epidemiological situation worsens. The Federal Council reinforces health measures. "Non-essential" shops, restaurants, leisure and sports facilities and cultural centres are closed. The ski resorts remain open, however, as do hotels and their facilities (restaurants, gyms, spas, etc.) available to their guests.

2021

February: The Federal Council opts for a phased exit from lockdown.

March: Reopening of all shops, museums, libraries, outdoor recreation areas.

April: Reopening of terraces, cinemas, theatres and football stadiums under strict conditions.

End of May: Restaurants and spas can reopen and public events can accommodate up to 300 people.

June: The conditions for entry into Switzerland are relaxed from 28 June. The entry ban is lifted for travellers from non-Schengen countries if they are vaccinated.

September: Fourth wave of COVID-19, gradual reintroduction of cantonal and federal health measures.

December: Enhanced enforcement of the indoor vaccination certificate and mandatory teleworking.

2.1.1 Demand in tourist accommodation

In 2021, tourist accommodation in Switzerland, which includes the hotel and supplementary accommodation sectors, recorded a total of 45.9 million overnight stays (G2.1.1), 19.1% more than in 2020. Compared with 2019, however, overnight stays were still 18.4% lower. In 2021, the hotel sector represented the largest share of demand with 64.4% of overnight stays recorded.

2.1.2 Swiss and foreign demand

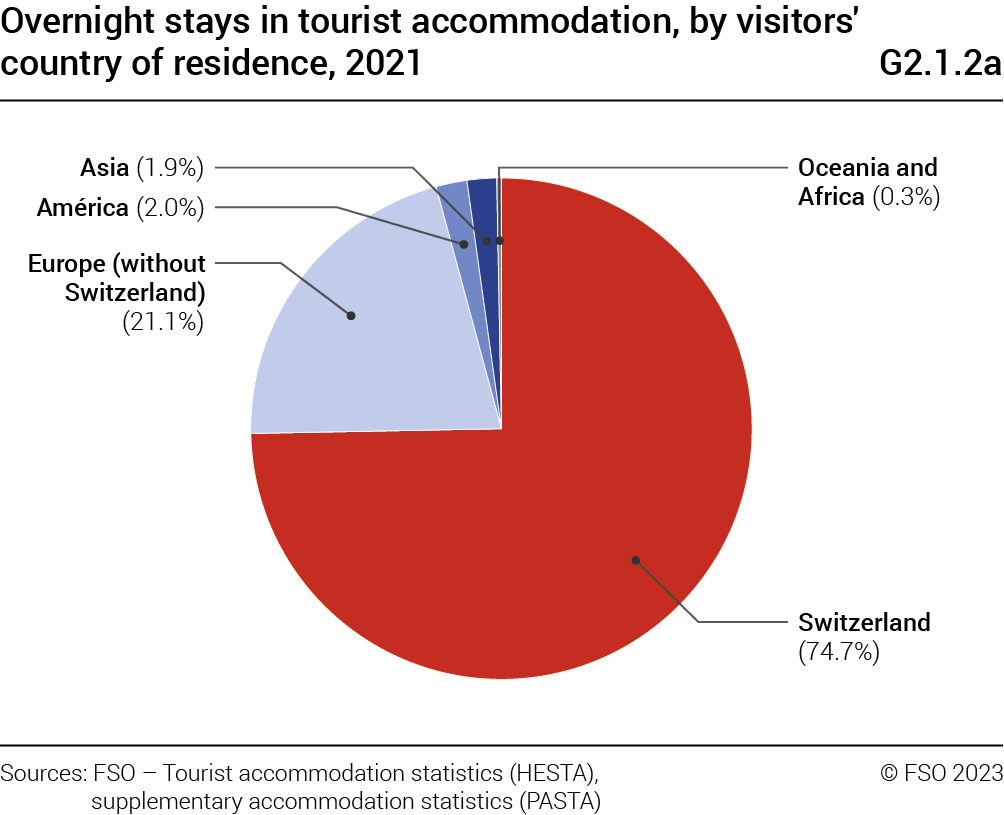

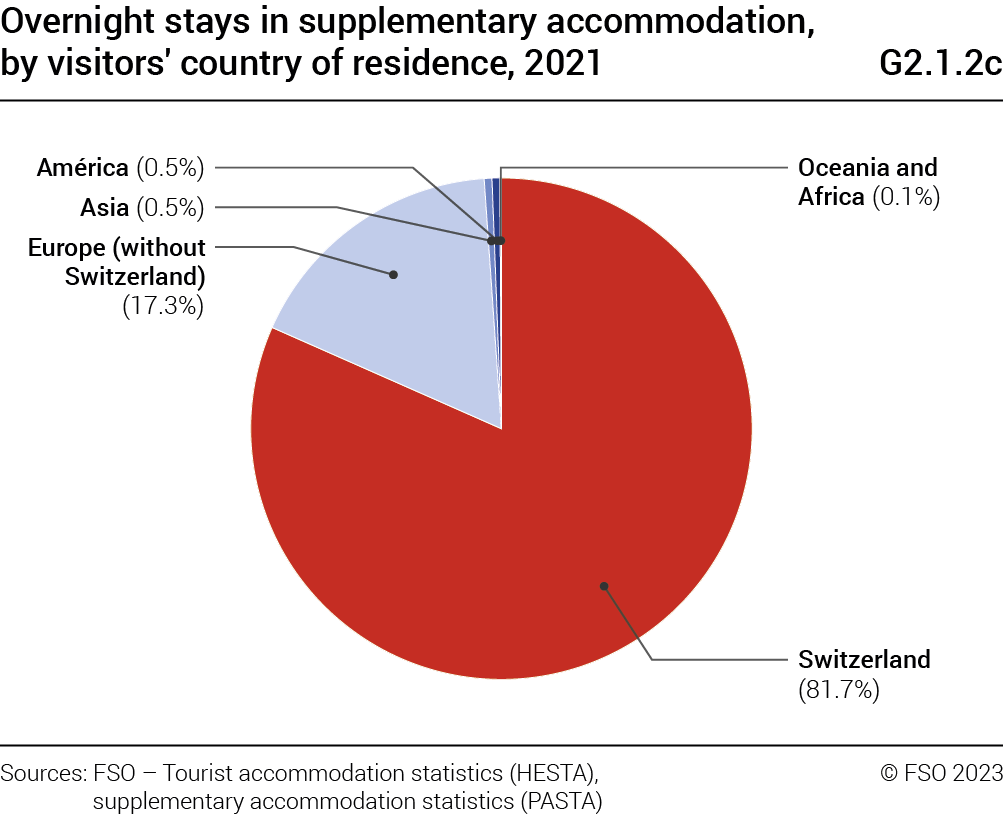

In 2021, Swiss clientele accounted for 74.7% of the overnight stays recorded in Swiss tourist accommodation (G2.1.2a). In 2020, Swiss demand fell only slightly (–3.7%). In 2021, overnight stays by this clientele increased sharply (+21.3%) and well exceeded the 2019 values (+16.8%). After a historic fall of 61.9% in 2020, foreign guests saw an increase again (+13.1%) in 2021. However, this remains well below the 2019 level (–56.9%). Within foreign clientele, European guests generated the most overnight stays in 2021 accounting for 21.1% of the total demand. The majority of demand in supplementary accomodation came from Swiss guests (81.7%) (G2.1.2c). This share is also in the majority in the hotel sector, although slightly lower (70.9%) (G2.1.2b).

Did you know?

The share of non-European overnight stays only represented 4.2% of the total demand in 2021 in tourist accommodation in Switzerland.

2.1.3 Breakdown for monthly demand

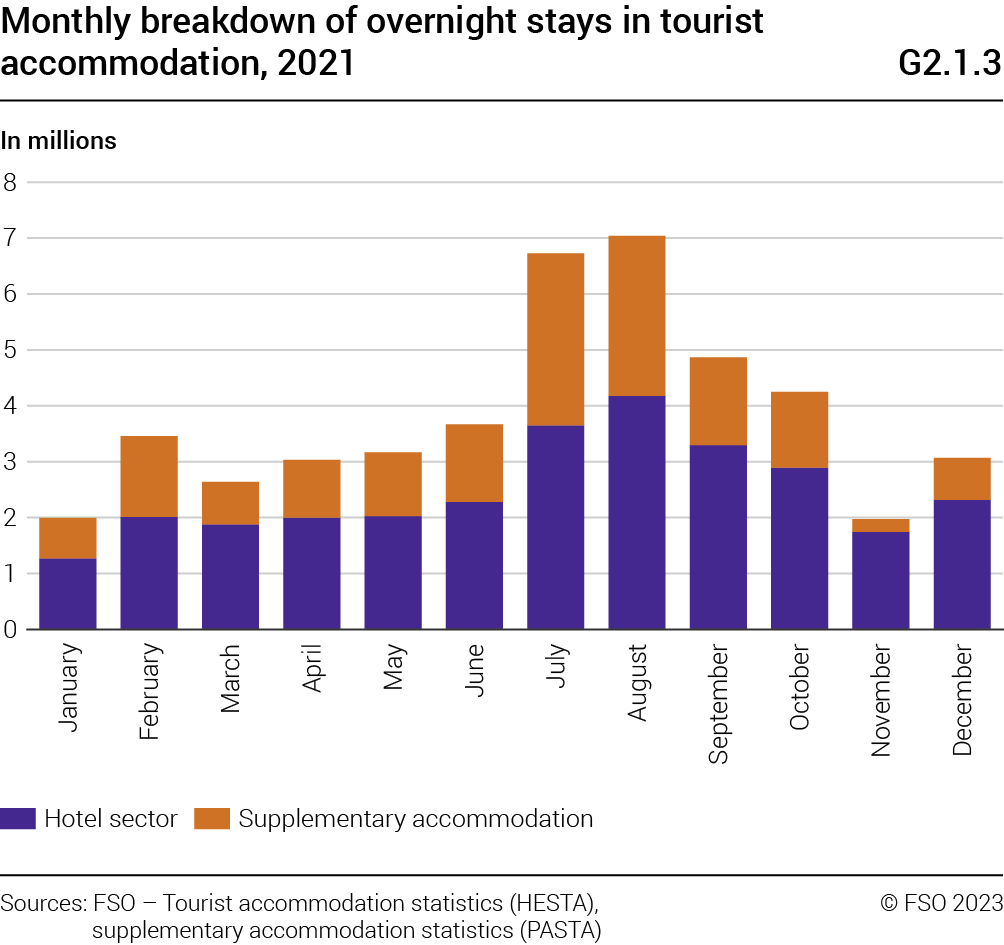

In 2021, the greatest number of overnight stays in tourist accommodation in Switzerland was recorded in the months from July to October (G2.1.3). 22.9 million overnight stays were counted in these four months alone, i.e. almost 50% of the annual demand.

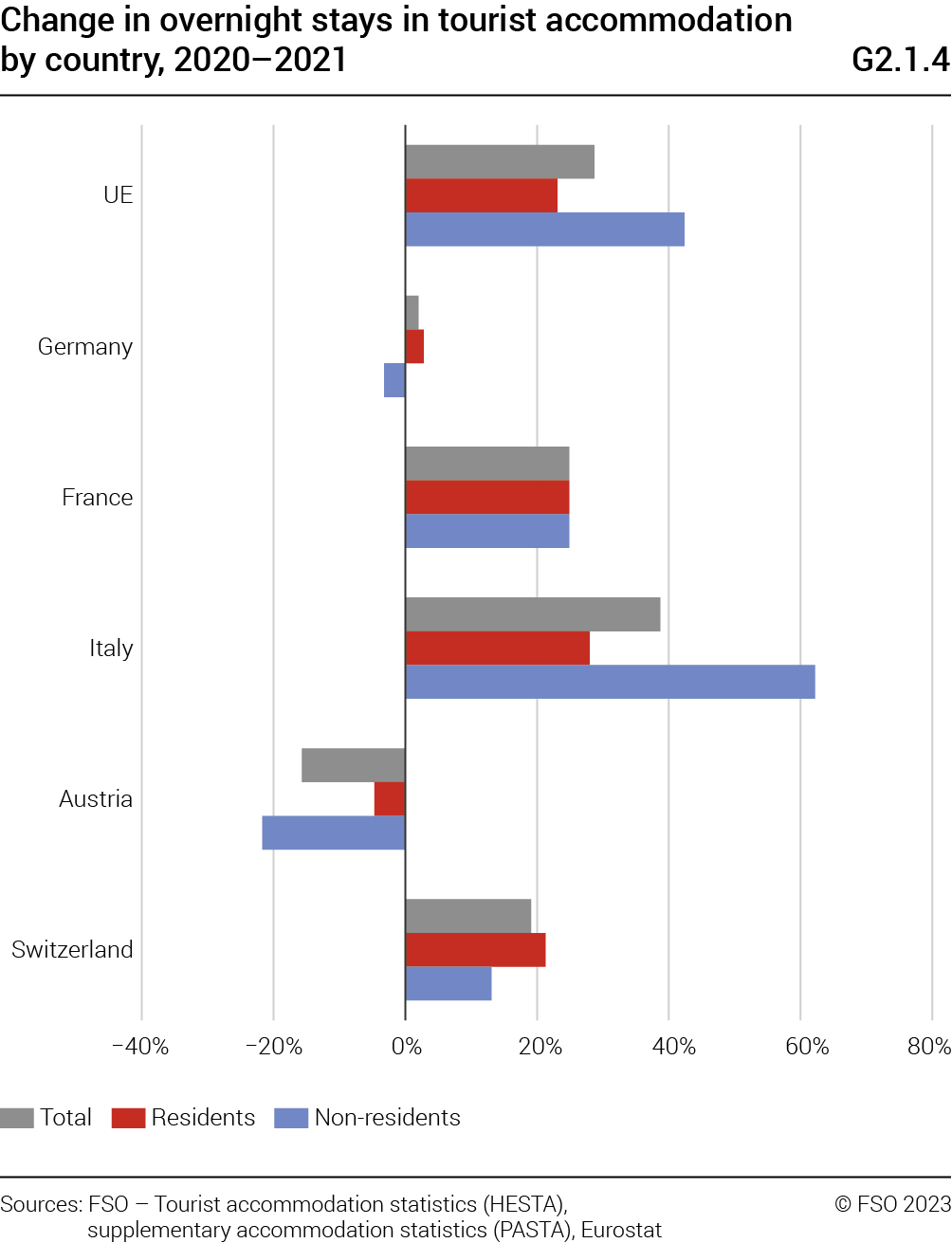

2.1.4 Change in demand in the countries neighbouring Switzerland

In comparison with the European results (EU), Swiss tourist accommodation in 2021 showed an analogue but nonetheless less marked development in overnight stays (G2.1.4) with an increase of 19.1% (versus +28.7% for the EU) compared with 2020. With the exception of Austria (–15.7%), all other neighbouring countries (Germany, France and Italy) also saw increases.

In 2021 at European level, the number of overnight stays generated by both non-residents and residents grew (+42.4% and +23.1% respectively, compared with 2020). For Switzerland, in contrast with the EU, non-residents' overnight stays showed a lower increase (+13.1%) than those of residents (+21.3%). France and Italy saw very strong increases for residents (+24.9%, respectively 28.0%) and non-residents (+24.9%, respectively +62.2%). In Germany, demand from non-residents fell (–3.2%), while demand from residents rose slightly (+2.8%). Finally, Austria saw a decrease for residents (–4.7%) as well as for non-residents (–21.7%).

2.2 Hotel sector results

2.2.1 Supply in 2021

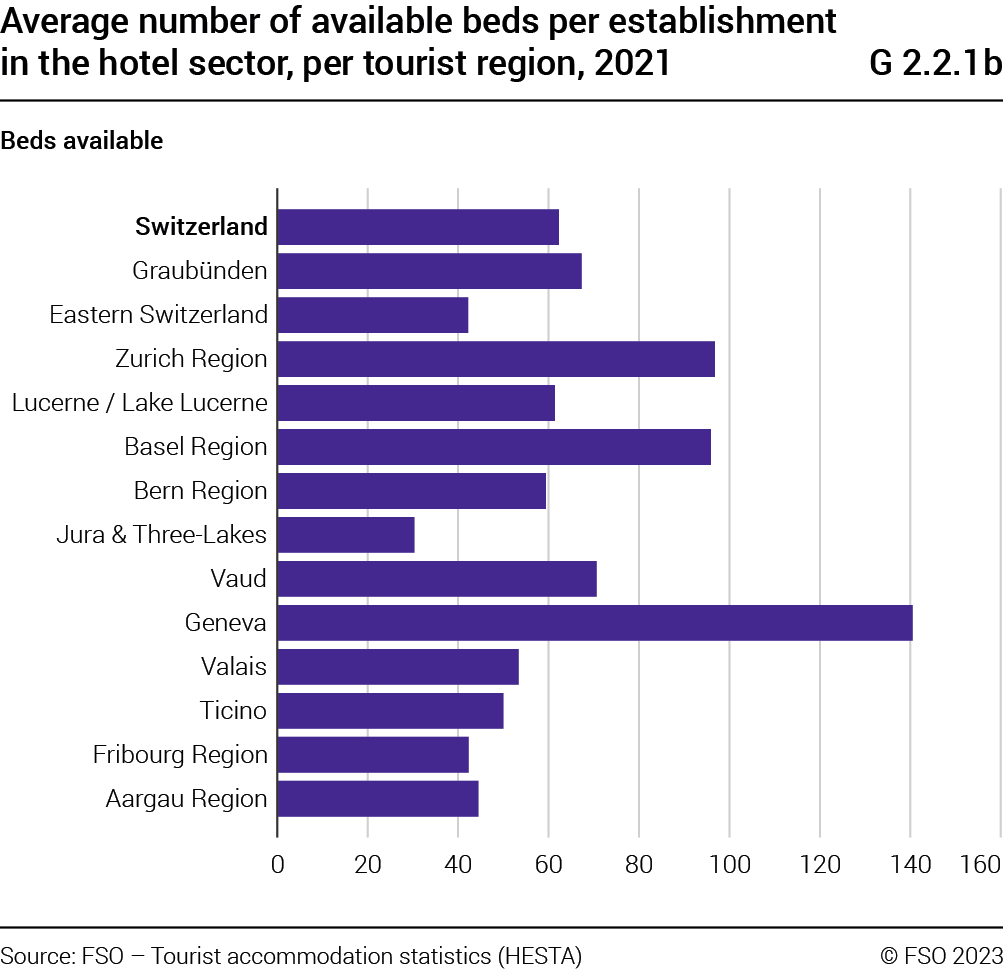

In 2021, there were, on annual average, 3919 open hotels and health establishments in Switzerland, corresponding to 124 590 rooms and 244 026 beds available (G2.2.1a). The number of open establishments in 2021 was slightly higher than in 2020 (3801) but still well below the number seen in 2019 (4234). Due to the COVID-19 crisis, a large number of establishments closed temporarily in 2020 and 2021. The distribution of establishments differed between tourist regions. In 2021, Graubünden had the largest proportion (14.8%), followed by the Bern Region (13.3%). The national average capacity of a hotel establishment was 62.3 available beds (G 2.2.1b).

Did you know?

In Geneva, an establishment had an average of 140.5 beds available in 2021, while in the Jura and Three Lakes region the average was only 30.3.

2.2.2 General change in supply

In 2021, a total of 4574 establishments and 142 743 rooms were surveyed in the hotel sector in Switzerland. The number of establishments decreased slightly in comparison with 2020 (–72 establishments / –1.6%) (G2.2.2a), whereas the number of rooms remained virtually stable (+86 rooms / +0.1%). At the level of the tourist regions, the supply, in terms of establishments, was down in ten out of thirteen regions between 2020 and 2021. In terms of rooms, eight out of thirteen regions recorded a lower number of rooms than in the previous year.

Over a comparative period of 10 years (G2.2.2b), the number of surveyed establishments diminished greatly. In 2012, the number of surveyed establishments totalled 5257 in Switzerland, corresponding to a decline over this period of 684 units (–13.0%). In terms of the number of rooms, an increase (+2370 rooms / +1.7%) can be observed for 2021. Over the same period, all tourist regions saw their supply in terms of establishments decrease. Eastern Switzerland registered the greatest decline with 133 fewer establishments (–11.7%). As far as rooms are concerned, only seven tourist regions showed an increase. The Zurich region showed the greatest growth (+3707 rooms / +22.7%). In contrast, the decline was most marked in Eastern Switzerland (–1215 rooms / –11.7%).

2.2.3 General trend in demand

To better appreciate the results of the demand in the hotel sector in Switzerland, these should be correlated with the striking economic events which have occurred over the past ten years.

The effects of the global economic crisis in 2009 had an impact on demand in the years that followed. At national level, 2011 was characterised by a strong rise in the Swiss franc's value against the Euro and other currencies. On 6th September 2011, the introduction of the minimum exchange rate by the Swiss National Bank (SNB) stabilised exchange rates, which nonetheless remained far lower than in previous years. On 15th January 2015, the SNB announced the end of the minimum exchange rate, resulting in renewed strength of the Euro compared with the Swiss franc. In the following two years, although the Euro regained some ground against the Swiss franc it never reached its pre-2015 level. From the end of February 2020, the pandemic completely changed society and the economy. Both the national and international tourism sectors were very negatively affected by this exceptional situation. Even if the measures against the pandemic in Switzerland and in many countries were somewhat reduced in 2021, the negative effects on the tourism sector were still very strong.

Over the past ten years, the evolution in the total number of overnight stays in hotels and health establishments in Switzerland has been diverse (G2.2.3a). After a decline in 2011, the number of overnight stays decreased again in 2012 (–2.0%). The trend was reversed for the years 2013 (+2.5%) and 2014 (+0.9%), however renewed decreases were observed for the years 2015 (–0.8%) and 2016 (–0.3%). A strong improvement in demand was seen in 2017 (+5.2%) which continued in 2018 (+3.8%) and in 2019 (+1.9%) with a total of 39.6 million overnight stays recorded, i.e. a level never seen before until now. In 2020, demand fell by a historic 40.0% to 23.7 million overnight stays. For the same year, with the exception of January (+7.1%) and February (+7.0%), very sharp monthly falls could be observed, ranging from –91.8% in April to –24.9% in July. Although the COVID-19 situation persists in 2021, the health measures are less severe than in 2020. 2021 therefore saw a recovery in demand and totalled 29.6 million overnight stays, an increase of 24.6%. While for the first two months of the year significant decreases in overnight stays were observed compared with the same period in 2020, demand increased strongly between March and June. The peak was reached in April with an increase of over 800%. These sharp increases can be explained by the particularly low demand the year before, period in which health restrictions were introduced and were at their strictest. In July, growth in demand slowed down (+6.4%) and then increased again very markedly between August and December to reach the levels seen in 2019.

2.2.4 Change in domestic and foreign demand

Looking back on the past 10 years, foreign and domestic demand in the hotel sector has not always followed similar trends (G2.2.4). In 2012, some discrepancies were observed. On the one hand, domestic demand was quite stable (–0.4%) while foreign demand showed a decrease (–3.3%). In 2013, however, a positive trend was observed for both types of demand. It continued in 2014. Whereas the increase in overnight stays for Swiss clientele continued in 2015 and 2016, demand from foreign clientele saw a decline once again. In 2017 and 2018 both foreign and domestic demand increased. This situation continued in 2019. Indeed, a rise of 1.1% was registered for foreign visitors and of 2.9% for Swiss visitors. The total overnight stays by foreign guests (21.6 million) as well as those by domestic guests (17.9 million) reached record levels in 2019. In 2020, foreign demand fell drastically to 7.3 million overnight stays (–66.1%), while domestic demand totalled 16.4 million overnight stays, which is a significant (–8.6% / –1.5 million) but less drastic decline. However, demand picked up again in 2021, especially for domestic customers (+27.9%), who far surpassed the record level of 2019 with a total of 21.0 million overnight stays. Foreign demand also increased (+17.1% ) but still remained far lower than that of 2019 with a total of 8.6 million overnight stays.

Following the year 2020 that was marked by a drastic fall in demand, the recovery observed in 2021 was characterised by monthly developments that were sometimes extreme (G2.2.4b).The months of January and February saw a decline in Swiss overnight stays (–36.9% and –2.9% respectively) compared with 2020. In March, domestic demand increased strongly (+106.1%); It exploded in April (+937.4%) and remained very strong in May (+198.7%) and in June (+49.9%). After a decline in July (–3.1%) that should be compared with the strong increase from the same month in 2020 (+35.0% compared with 2019), Swiss demand rose again until December. Peak growth was recorded in April (+937.4%). For foreign guests, the months of January and February 2021 were strongly negative (–79.8% and –79.4%). While it still decreased in March (–27.2%), foreign demand exploded in April and May (+466.9% and +324.6% respectively). Between June and September, it continued to increase but less substantially than in previous months. The last three months of the year once again showed more pronounced increases (+169.1% in October; +276.6% in November and +167.8% in December).

Did you know?

In 2021, Swiss demand reached an all-time high with an increase of 17.0% compared with the previous record in 2019.

2.2.5 Change in demand by continent of origin of guests

In 2021, demand from Europe (excluding Switzerland) registered 6.9 million overnight stays, representing an increase of 13.7% (+82

Ne pas séparer le chiffre

8 000 overnight stays) compared with 2020 (G2.2.5a). This increase is linked to the shorter and less severe health measures than in 2020: The level of overnight stays in 2021 for this clientele was still much lower than in 2019 (–44.0%). The biggest contributor to this growth in 2021 was Germany (+369 000 nights / +16.5%). It should also be noted that overnight stays by guests from the United Kingdom continued to fall, with a drop of 190 000 nights (–36.2%). Following the global economic crisis in 2009 and the strong appreciation of the Swiss franc against the euro in 2011, demand from the European continent fell steadily until 2016. It then stagnated until 2019 and never recovered to its pre-2009 level.In 2021, demand from Asian visitors for hotels also recovered (G2.2.5c). A total of 794 000 overnight stays were observed for this clientele, i.e. an increase of 35.3% (+207 000 nights) compared with 2020. This growth was mainly attributable to the Gulf countries which showed an increase of 312 000 overnight stays (+273.9%). Despite this recovery, the level of overnight stays by Asian visitors was still much lower than in 2019 (–85.4%). The arrival of COVID-19 in 2020 ended a decade marked – in general – by strong annual growth for visitors from this continent.

Finally, there was also an increase in demand from guests from the American continent (+256 000 nights / +44.2%) and from the African continent (+12 400 / +15.5%). Only clientele from Oceania showed a decline compared with 2020 (–46 000 / –69.3%). Here too, the demand for these continents in 2021 remained significantly lower than in 2019.

Did you know?

Between 2019 and 2021, overnight stays by guests from China fell by 97.4% from 1.4 million units to 36 000.

2.2.6 Change in demand by tourist region

In 2021, Switzerland’s thirteen tourist regions observed increases in overnight stays compared with 2020 (G2.2.6). The greatest increase was seen in Ticino (+51.8%). The city regions follow closely with Geneva (+46.3%), the Basel Region (+39.3%) and Zurich region (+39.1%). The smallest increases were seen in Valais (+8.6%) and Graubünden (+8.0%). Compared with 2019, only Ticino (+27.1%) and Jura and Three Lakes (+1.3%) registered more overnight stays in 2021.

In terms of domestic demand, all tourist regions showed an increase in results ranging from +12.1% for Graubünden to +54.9% for Ticino. Compared with 2019, only four regions saw their overnight stays decrease in 2021. The largest decreases were observed in the city regions. In terms of foreign demand, eleven out of thirteen tourist regions recorded an increase ranging from +10.3% (Bern region) to +41.8% (Geneva). Only Graubünden (–4.5%) and Valais (–11.8%) saw their overnight stays decrease. Compared with 2019, all tourist regions saw a strong decrease in foreign demand in 2021.

Did you know?

Ticino recorded its highest number of overnight stays in 2021 for 20 years.

2.2.7 Duration of stay

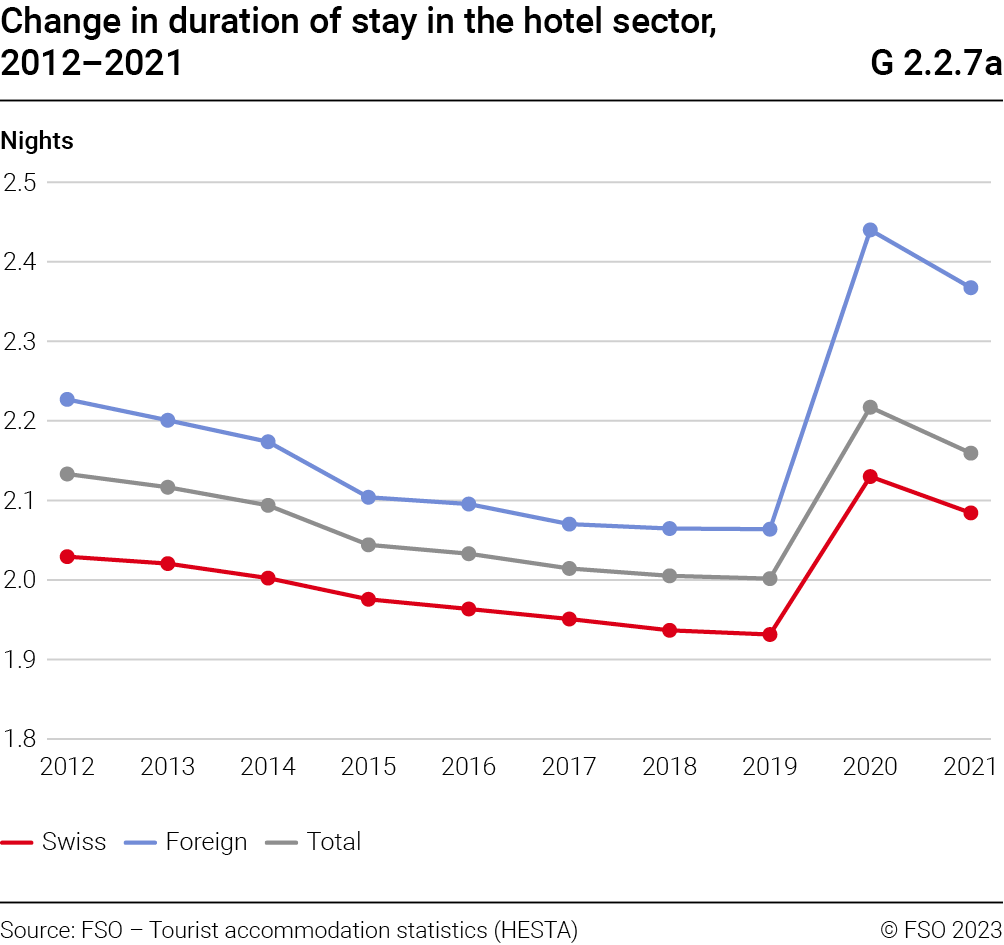

In 2021, visitors stayed an average of 2.16 nights in hotels and health establishments in Switzerland. This duration was, however, longer for foreign visitors (2.37 nights) than for Swiss visitors (2.08 nights).

Although the results for 2021 were slightly lower than for 2020, they are still higher than those observed over the previous ten years (G2.2.7a). This is mainly due to the fact that in 2021 the native population still favoured holidays in Switzerland in view of the health situation.

Among the tourist regions, Graubünden recorded the longest stay in 2021 with 2.76 nights (G2.2.7b). In contrast, the shortest length of stay was observed in the region of Fribourg (1.67 nights). As at national level, the length of stay was longer for foreign clientele than it was for domestic visitors in all tourist regions excluding Ticino. The greatest difference was observed in Graubünden where foreign visitors stayed for an average of 3.37 nights whereas Swiss visitors stayed for 2.63 nights.

2.2.8 Occupancy rate of rooms

In 2021, the net room occupancy rate was 41.4% (G2.2.8), an increase of 5.4 percentage points compared with 2020. However, this remained well below the 2019 level (55.2%). Of the thirteen tourist regions, only Valais (46.2% / –1.9 points) saw a decrease in occupancy. Ticino recorded the highest rate (59.4% / +14.6 points). It is also the only region to have a higher occupancy rate than in 2019. Despite rising rates, the city regions of Zurich (34.0% / +6.9 points), Geneva (34.2% / +7.7), and Basel (34.4% / +6.4) had the lowest values. The rates for these regions were far off the high levels of 2019 (66.5% for Geneva); 65.0% for the Zurich region and 60.1% for the Basel region).

2.2.9 Change in demand in the countries neighbouring Switzerland

In the EU in 2021, overnight stays in the hotel sector increased by 30.6% (G2.2.9). An increase could also be observed in Switzerland (+24.6%) as well as in the countries neighbouring Switzerland, except for Austria which experienced a decrease of 16.3%.

In Switzerland, a substantial increase in overnight stays was seen by both residents (+27.9%) and non-residents (+17.1%) Demand from residents (+24.3%) and non-residents (+44.3%) increased strongly in the EU, as in France and Italy. Germany showed only a small increase for non-residents (+0.3%) and residents (+2.7%), while Austria showed a decrease for non-residents and residents (–22.0%, respectively –5.6%).

2.3 Supplementary accommodation results

In the supplementary accommodation sector, the statistic covers three main types of accommodation: commercially-run holiday homes, collective accommodation and campsites. In order to present information from the supplementary accommodation sector as comprehensively as possible, the results are broken down by each type of accommodation.

2.3.1 Supply in supplementary accommodation

A) Holiday homes

In 2021, a total of 29 438 commercially run holiday homes were counted in Switzerland (G2.3.1a). This represents a capacity of 143 196 beds. If we consider the distribution of holiday homes by Switzerland’s seven major regions, the Lake Geneva Region has the largest share with 46.0% of the total. This was followed by Eastern Switzerland with a share of 27.5%.

B) Collective accommodation

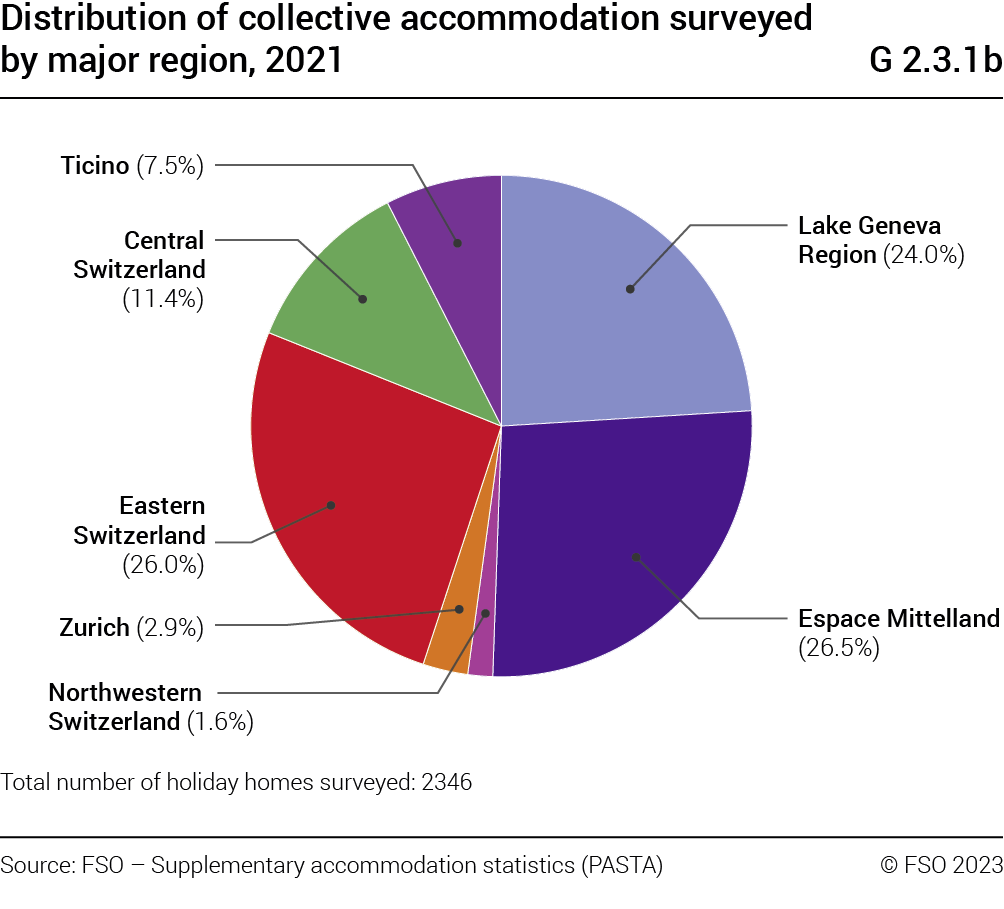

At national level, there were 2346 collective accommodation units, i.e. a total of 113 155 beds were surveyed for the year 2021 (G2.3.1b). At major region level, Espace Mittelland had the greatest share of establishments (26.5%) closely followed by Eastern Switzerland (26.0%) and the Lake Geneva region (24.0%).

C) Campsites

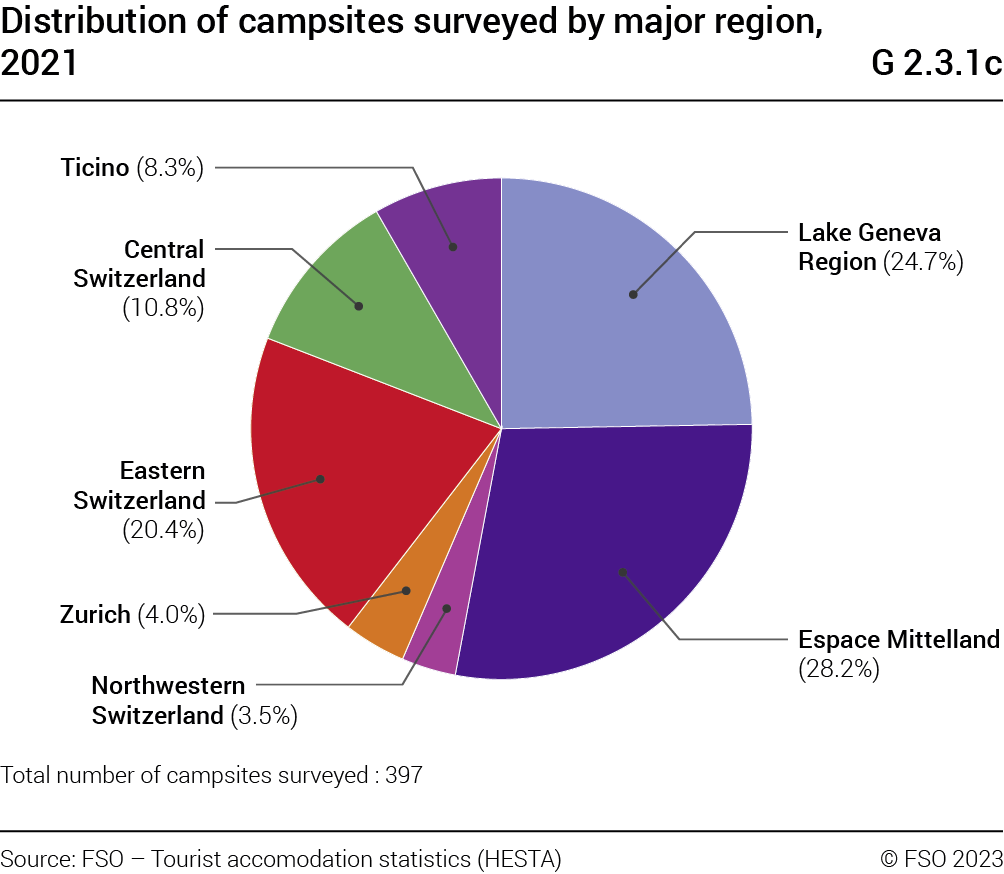

The total number of campsites surveyed in Switzerland in 2021 was 397, i.e. 28 457 rental pitches for passing guests (G2.3.1c). In terms of distribution at major region level, Espace Mittelland (28.2%) and the Lake Geneva region (24.7%) recorded the largest number of establishments.

2.3.2 Demand in supplementary accommodation

A) Holiday homes

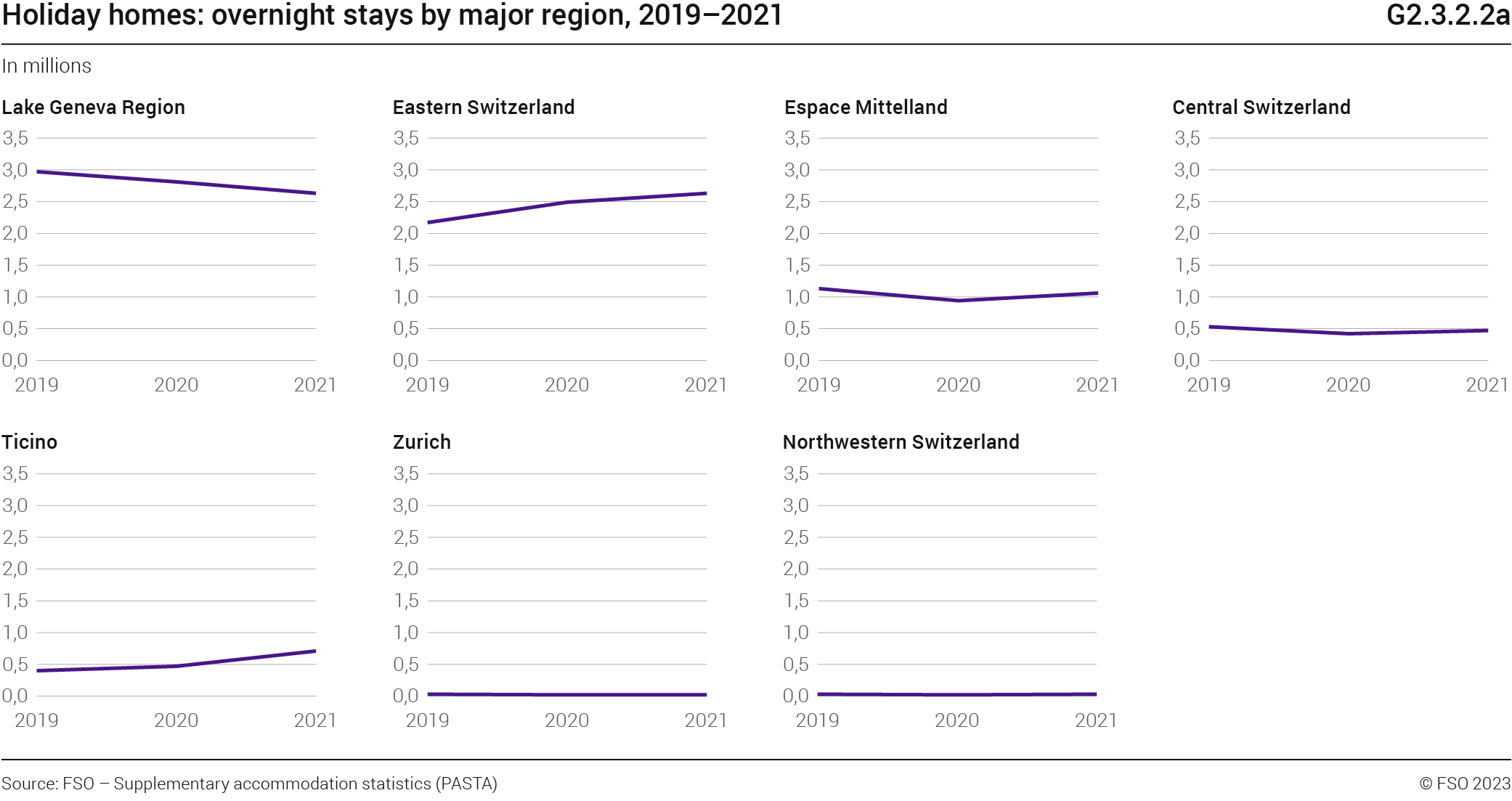

Commercially-run holiday homes accounted for the majority of overnight stays in supplementary accommodation in 2021 with 46.3%. At 7.6 million overnight stays (G2.3.2.1a), demand has increased by 5.5% compared with 2020, exceeding that of 2019 (7.3 million). Domestic demand generated 5.9 million overnight stays (+8.5% compared with the previous year), foreign demand 1.6 million (–4.1%). Guests from Europe accounted for over 90% of overnight stays (–8.5%). Among the seven major regions, the Lake Geneva region and Eastern Switzerland saw the strongest demand with a total of 2.6 million overnight stays each (G2.3.2.2a).

B) Collective accommodation

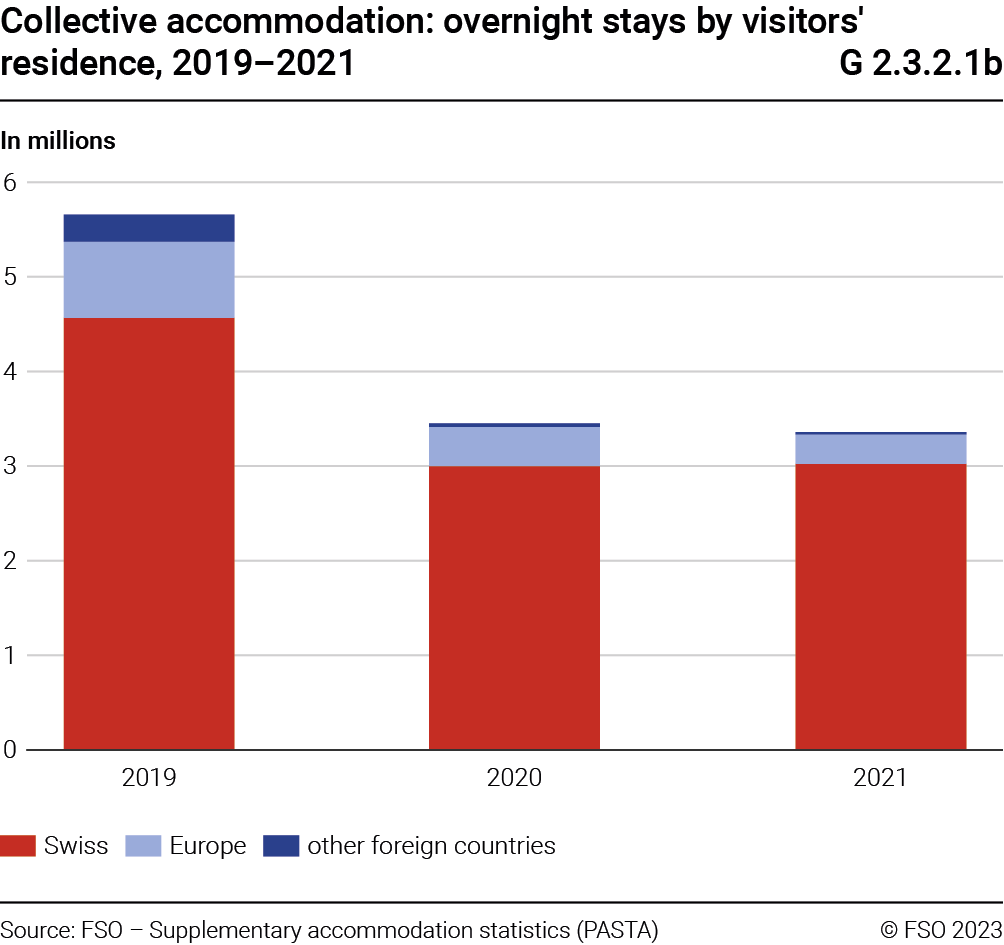

The 2.6% drop to 3.4 million overnight stays in collective accommodation in 2021 (G2.3.2.1b) is the consequence of the 81.5% drop in the first quarter compared with the same quarter of 2020, which was still relatively unaffected by the pandemic. Over the whole year, the number of overnight stays decreased by 40.6% compared with 2019. Domestic guests generated 3.0 million overnight stays, an increase of 0.7%. Foreign clientele (92.7% from Europe) generated 338 000 of these stays (–24.9%). At the level of the major regions (G2.3.2.2b), Espace Mittelland had the highest number of overnight stays (830 000).

C) Campsites

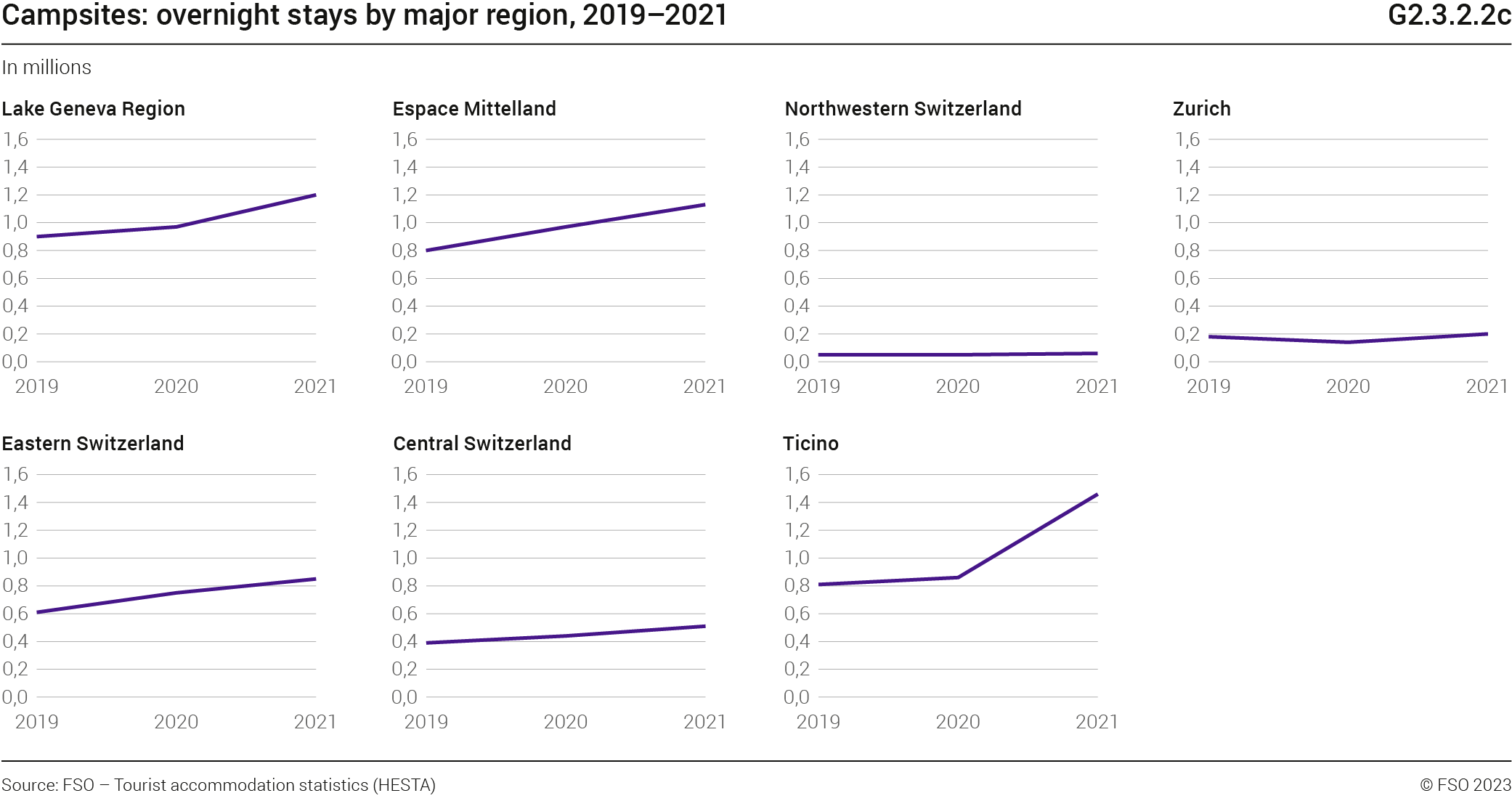

In 2021, with 5.4 million overnight stays (+29.7% compared with 2020), a new record was reached for campsites (G2.3.2.1c). The number of overnight stays increased by 44.1% compared with 2019. Both domestic and foreign demand showed strong increases (+28.6% and +34.3% respectively). Compared with 2019, the decline in foreign visitors (–15.1%) was more than offset by the increase in domestic demand (+72.2%). Ticino was the major region (G2.3.2.2c) where campsites recorded the most overnight stays (1.5 million), followed by the Lake Geneva Region (1.2 million).

Did you know?

In 2021, European visitors accounted for 99.0% of foreign demand at campsites.

2.3.3 Breakdown for monthly demand

A) Holiday homes

Visits in terms of overnight stays in holiday homes (G2.3.3a) were concentrated mainly in February (17.1% of annual demand) and in July and August (28.4%). November represented only 1.4% of the total demand.

Did you know?

In holiday homes, February alone accounted for 17.1% of the annual number of overnight stays in 2021.

B) Collective accommodation

The monthly breakdown of demand in collective accommodation in 2021 highlighted the fact that overnight stays were mainly generated in the summer, more precisely between July and October (G2.3.3b) and at the begining of autumn. These four months accounted for 68.1% of annual overnight stays. The period from January to March represented only 7.1% of the total overnight stays.

Did you know?

In collective accommodation, July alone accounted for 22.1% of the annual number of overnight stays in 2021.

C) Campsites

Showing strong seasonal variation, demand in campsites was unsurprisingly almost entirely concentrated over the summer period (G2.3.3c). Almost 80% of overnight stays (80.8%) were recorded between May and September.

2.3.4 Duration of stay in supplementary accommodation

A) Holiday homes

The average length of stay in holiday homes in Switzerland reached 6.52 nights in 2021 (6.60 in 2020) (G2.3.4a). However, this value varied by major region. Indeed, in Ticino it was 6.74 nights (6.37) and in Eastern Switzerland it was 6.73 nights (7.00), i.e. the longest durations at this regional level. In contrast, the Northwest Switzerland region registered the shortest value of 4.52 nights (5.05).

B) Collective accommodation

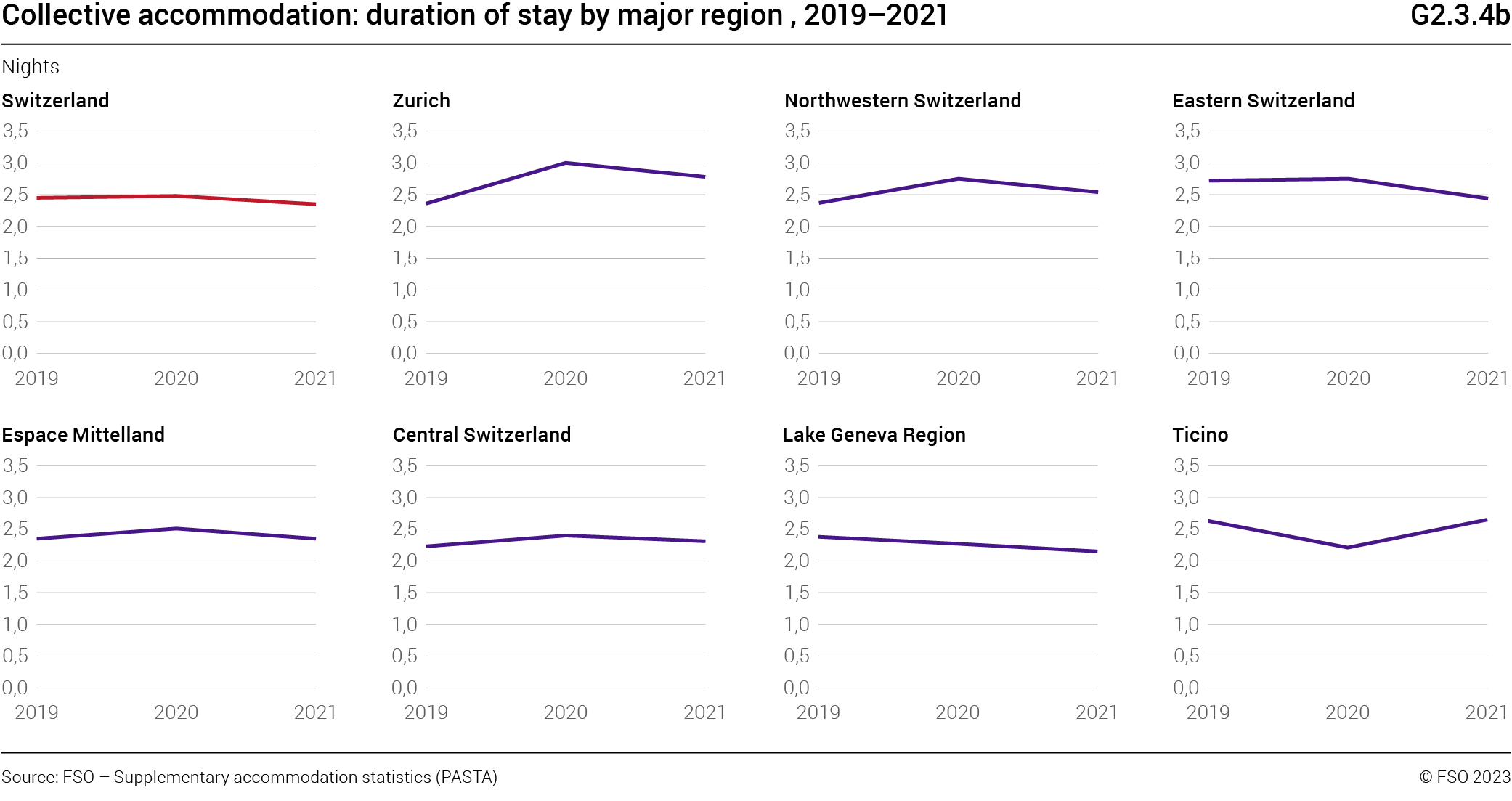

In 2021, the average length of stay in collective accommodation nationally was 2.35 nights (2.48 in 2020) (G2.3.4b). Among the major regions, Zurich registered the longest stay with 2.78 nights (3.00). Conversely, the shortest length of stay was seen in Lake Geneva with 2.15 overnight stays (2.27).

C) Campsites

For campsites, the average length of stay in 2021 was 3.21 nights (3.16 in 2020) for Swiss territory (G2.3.4c). This duration reached 3.99 nights (3.88) in Ticino, i.e. the highest among all the major regions. The shortest length of stay was in Zurich with 1.94 nights (2.00).

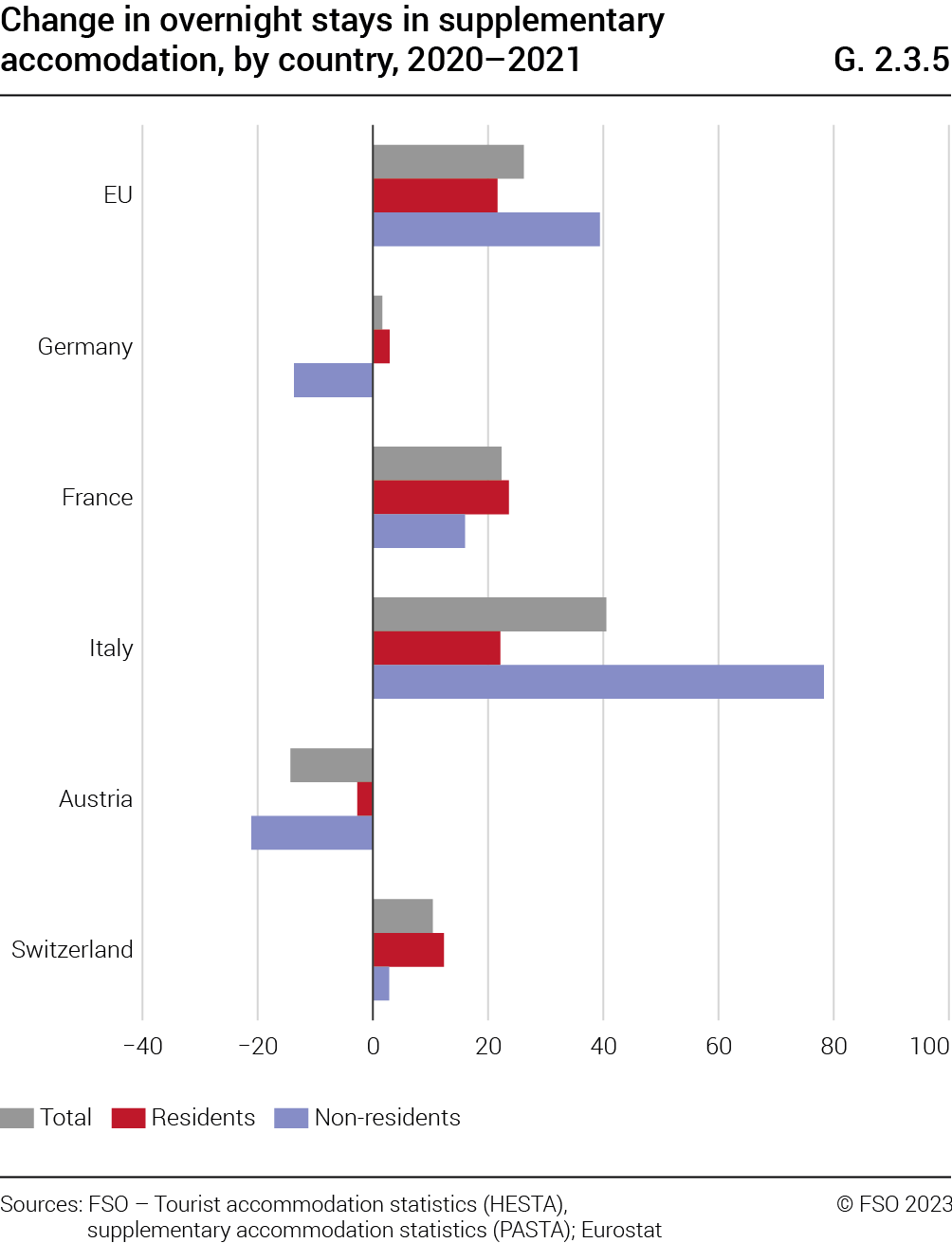

2.3.5 Change in demand in the countries neighbouring Switzerland

The trend in overnight stays in the EU in the supplementary accommodation sector increased by 26.2% (G2.3.5). Switzerland recorded an increase in demand of 10.4%, less than Italy (+40.5%) and France (+22.3%), but more than Germany (+1.6%). Austria (–14.3%) was the only country neighbouring Switzerland to experience a drop in overnight stays compared with 2020.

Overnight stays by residents in the EU increased by 21.6% and those of non-residents by 39.4%. For Switzerland, demand from residents (+12.3%) showed a more marked increase than that from non-residents (+2.8%). As for the other countries bordering Switzerland, the increases were significant for France (+23.6% for residents and +16.0% for non-residents) and Italy (+22.1%, respectively, +78.3%). For Germany, residents showed a slight increase (+2.9%), while non-residents showed a decrease of 13.7%. Austria, on the other hand, saw a decline for residents and non-residents (–2.7% and –21.1% respectively).