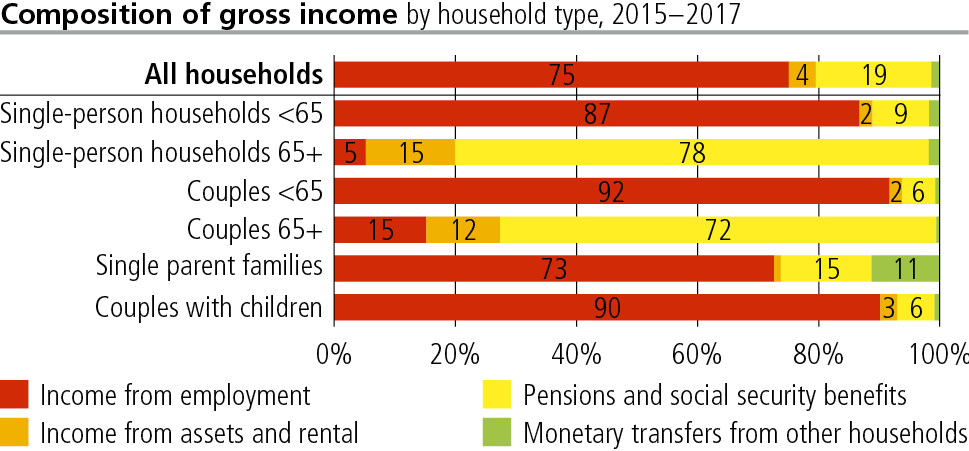

Household budgets: Income

Averaged out over all households, income from employment at 75% represents the main component of household income. The second important component consists of pensions from the first and second pillars of the Swiss pension system and other social security benefits at 19%. The remainder of household income is made up of income from assets and transfers from other households.

The picture becomes more differentiated when the composition of household income is considered by household type. This shows, for example, that in households aged 65 and over, pensions represent the major part of the household income, but income from employment and, in particular, income from assets play a relatively important role.

Transfers from other households represent an important source of income only in specific types of households, such as single-parent families, where the average amounts to 11%.

Household budgets: Expenditure

The variations in the composition of spending are less pronounced. Compulsory deductions, which comprise 29% of gross income, are the largest item. In the area of consumer expenditure, the largest item is expenditure on housing at 15%. Other large items include expenditure on food and non-alcoholic drinks, on transport and on entertainment, recreation and culture.

After all expenditure has been deducted, on average 15% of the gross income is left for saving. There are significant differences in this area depending on household type. Households over the age of 65 on average save less than younger households. Sometimes this figure is even a minus, which means that these households are living on their capital, among other things.

Household expenditure over time

The composition of household expenditure has changed significantly over time. These changes are considerably larger than the differences between households today. For example, the share of total expenditure represented by expenditure on food and non-alcoholic drinks in 1945 was 35%, but nowadays this has fallen to 7%. In contrast the proportion of other expenditure has increased, such as expenditure on transport, which has risen from around 2% to 8%.

Availability of consumer goods

Information about the availability of a selection of durable consumer goods shows that households in Switzerland are very well-equipped with IT hardware. A total of 96% of people live in a household with a computer and 98% in a household with a mobile phone. These proportions are continuing to rise: in 1998 only 55% of people lived in a household with a computer.

In the case of household appliances, such as dishwashers, washing machines and tumble dryers, there has also been an increase. In 2018, 88% of the population lived in a household with a dishwasher, while in 1998 the figure was only 61%.

Material deprivation

The reasons for not owning a durable good are not necessarily financial. In 2018, less than 2% of people living in Switzerland went without a computer for financial reasons; as far as owning a car for private use is concerned, this percentage was 5%. One of the most common material deprivation is caused by a lack of financial reserves. 20.7% of the population living in private households did not have the means to meet unexpected expenses of CHF 2500. This is followed by deprivation which affects the perceived inconveniences with regard to the residential environment. 17.2% of the population say that they are exposed to noise from neighbours or the street, 7.9% are confronted with problems of crime, violence or vandalism and 9.9% with a too wet accomodation. In addition, 9.6% of the population could not afford a week’s holiday away from home each year.

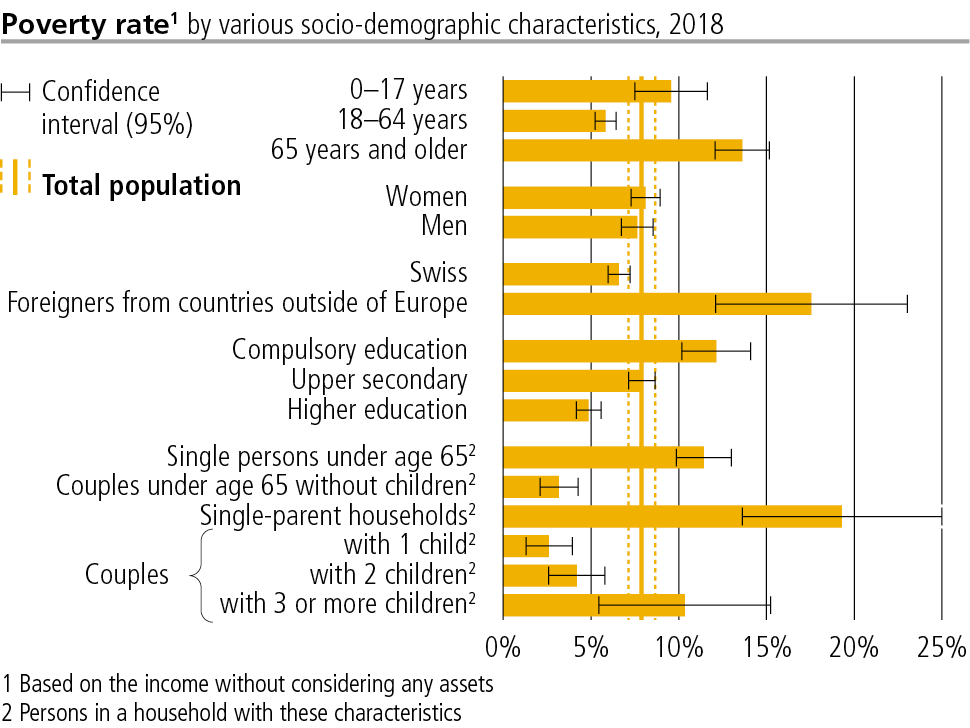

Monetary poverty and risk of poverty

In 2018, 7.9% of the permanent resident population in private households in Switzerland was affected by income poverty. This corresponds to approximately 660 000 persons. The average poverty threshold, based on the social subsistence level, was CHF 2286 per month for a single person and CHF 3968 per month for two adults with two children. According to the relative at-risk-of-poverty concept, 13.9% or some 1 165 000 persons were at risk of poverty. The at-risk-of-poverty threshold for a single person was CHF 2495 per month for a single person (60% of the median of the equivalent available income) and CHF 5240 for two adults with two children.

Poverty of employed persons

People living in households with high labour participation tend to have the lowest poverty rates. Successful integration in the labour market generally offers effective protection from poverty. Nevertheless, in 2018 some 3.7% or approximately 133 000 individuals were affected by poverty despite being in employment.

The phenomenon of working poverty is best understood in relation to the (longer term) security and insecurity of the employment situation. If working conditions and methods can be considered as clearly or tending to be insecure, the risk of poverty is greater.

Inequalities in income distribution

Inequalities in income distribution are assessed on the basis of equivalised disposable income. This is calculated as follows: A household’s compulsory expenditure is deducted from the household’s gross income; the resulting balance is divided by the equivalent size of the household. Thus the equivalised disposable income acts as an index of people’s standard of living, regardless of the type of household in which they live. In 2018, the equivalised disposable income of the wealthiest 20% of the population was 4.3 times greater than that of the poorest 20%.

► www.statistics.admin.ch → Look for statistics → Economic and social situation of the population